Summary

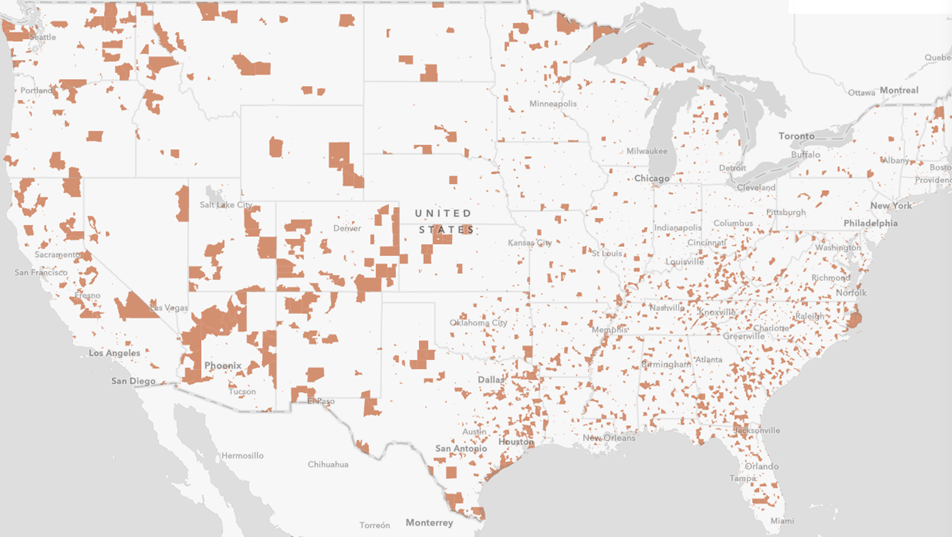

As part of the Tax Cuts and Jobs Act of 2017 (TCJA), a new community and economic development program was enacted under Section 1400Z-1 & 1400Z-2 that garnered little attention at the time of passage, but which now appears to be causing high net worth investors and the investment community at large to take notice. Qualified Opportunity Zones (QOZ’s), which currently include approximately 8,700 areas, located in all 50 states, U.S. territories and the District of Columbia , offer a tax subsidized investment opportunity for taxpayers that wish to reinvest their capital gains (See Map & Listing).

For those that have such capital gains, the types of investments that will be available to be made in QOZ’s could include the following properties and businesses:

- Real or personal property located in QOZ’s including commercial real estate development and renovations;

- New Businesses established and operating in QOZ’s which could include manufacturing, wholesale, warehousing & distribution or retail businesses;

- Expansion of Existing Businesses into QOZ’s; or

- Additional Investment in Expansions of Businesses or Property currently located in QOZ’s.

This opportunity provided by Congress, with the enactment of the TCJA, allows certain taxpayers to reinvest their capital gains into a Qualified Opportunity Zone Fund (QOF) and defer any U.S. income or capital gains taxes until no later than December 31, 2026. In addition, where the investment in the QOF is held for specified periods, taxpayers can receive a partial reduction of such capital gains when the investment is disposed of or the deferral period ends.

As an additional incentive for investing in such underdeveloped areas, if the investment in the QOF is held for period of at least 10 years, any appreciation of the interest in the QOF is never subject to U.S. taxation.

In Depth

Highlights of this tax-advantaged investment opportunity are set forth below:

Benefits of Investing in QOF:

The primary benefits available to a taxpayer that reinvests their capital gains into a QOF are the deferral of tax on such gains as well as the elimination of tax altogether on both a portion of the original gain invested and any gains recognized on the QOF investment itself. These benefits are summarized as follows:

Deferral and Partial Elimination of Tax on Initial Capital Gain:

- To qualify for the QOF incentive, taxpayers must invest their gains from the sale of capital assets in a QOF within 180 days after the sale. This can include both short term and long term capital gains as well as gains from Section 1231 and 1250 property.

- Despite the contribution of cash to the QOF, the investor will be initially deemed to have a tax basis of zero in the QOF.

- If the investor holds their interest in the QOF for at least 5 years, they increase their basis in the QOF by 10% of the deferred capital gain (resulting in the tax on 10% of the deferred gain being eliminated)

- If the investment in the QOF is held for at least 7 years, the investor’s basis is increased by an additional 5% of the deferred gain (resulting in a total of 15% of the tax on the deferred gain being eliminated).

- The tax on the capital gain invested in the QOF will be deferred until the earlier of December 31, 2026 or the date the investor sells their interest in the QOF. At the end of the deferral period (i.e. earlier of date of sale or December 31, 2026), if a taxpayer still holds its interest in the QOF, they must include in income the lesser of:

- the eligible gain that the taxpayer rolled-over less the gain (basis step-up) excluded if the taxpayer held its interest in the QOF for at least 5 or 7 years, OR

- the excess of fair market value of the taxpayer’s QOF investment over their basis in the QOF as of the end of the deferral period.

- It should be noted that based on the deferral rules referenced above, since the deferred gain will be taxed by no later than December 31, 2026 and because the investment in the QOF must be held at least 7 years in order to obtain the maximum 15% step-up in basis (gain elimination), an investment in a QOF should be made on or before December 31, 2019, to maximize the benefits.

Total Elimination of Tax on QOF Investment:

- Where the investment in the QOF is held for 10 years or more, the investor may elect to increase the basis in the investment to the fair market value on the date the investment is sold, thereby permanently eliminating any tax on the gain from the disposition of the QOF interest.

- This step-up in basis election on the QOF is only available where a gain deferral election was made on the original capital gain reinvested in the QOF.

- The designations of all QOF’s will expire on December 31, 2028, but the proposed regulations allow taxpayers to continue to make the 10-year basis step up election until December 31, 2047.

Eligibility for Investment in QOF:

Taxpayers eligible for the QOF benefits include individuals, C Corporations, S Corporations, Partnerships, RICs, REITs, and other pass-through entities as well as certain trusts or estates that have or will be recognizing capital gains.

All or a portion of a taxpayer’s capital gain income for a given year can be contributed to the QOF. There is no tracing of proceeds for this purpose and the gain can be divided into separate QOF investments and deferral elections. The investment must be in the form of equity (not debt) but such equity can be leveraged or used as collateral for loans to the QOF. Acquiring a QOF interest from another owner of the QOF interest does not qualify for QOF benefits. The investment in the QOF must occur within 180 days of the sale of the capital gain property.

The initial capital gain that is reinvested in a QOF retains its character throughout the deferral period (i.e. if short term gain rolled over it will be short term when eventually recognized). While the statute is silent on the issue, the current consensus is that when the deferral period has ended and the gain must be recognized, it will be taxed at the applicable rate at such time and not at the rate in effect when initially deferred. Further clarification by the IRS with regard to this result is warranted but not necessarily forthcoming. If a taxpayer dies during the deferral period, the gain is still recognized pursuant to the rules set forth above but there is no step up in basis of the property which is available in a customary bequest of property.

Partnerships/Flow-Throughs: For partnerships or other flow-through entities (i.e. S Corps, estates & trusts) that recognize a capital gain in a tax year, such entity may elect to defer gain by investing in a QOF directly or if it does not make such election, its partners may elect to reinvest their pro rata allocation of the gain into a QOF. Where a flow-through rolls over the gain directly into a QOF, it must be done within 180 days of the flow-through’s sale of the property. However, if the flow-through does not reinvest the gain directly, and an individual partner, shareholder or beneficiary (not every partner must elect) elects to reinvest their portion of the gain in a QOF, the general rule is that the 180 day period starts on the last day of the partnership’s tax year unless the partner is aware of the sale and elects to use that date to start the 180 day period.

Establishing & Operating a QOF:

To qualify as a QOF, 3 tests must be fulfilled which relate to organization, purpose, and assets of the QOF. If these requirements are met, the QOF self-certifies its status by attaching IRS Form 8996 to the QOF’s tax return beginning with the first year of the QOF and for each year thereafter that such status is maintained. The following sets forth the application of these eligibility rules:

Organization: The QOF entity must be organized as a corporation (although not specifically identified in the statute, S Corporations should also qualify as QOF’s) or partnership, which can include LLC’s treated as partnerships for tax purposes (the QOF Entity). A pre-existing entity can self-certify and establish a starting date as a QOF if all other qualifications are met (more specifically the asset test below). The form of the equity investment may include preferred shares or a partnership interest with special allocations. Additional capital may be invested (i.e. return of principal portion of the initial capital gain property), but will not be eligible for the exemption of tax on appreciation of the QOF.

Purpose: The purpose of the corporation or partnership electing to be characterized as a QOF must be formed as an investment vehicle for the purpose of investing in QOZ property and should be reflected in the documentation of the QOF.

Assets: The QOF Entity must hold at least 90% (which includes the cost of any land) of its assets in “QOZ property” based on an averaging of such asset’s values at the end of the first 6 months of the taxable year and at the end of the taxable year. Where a calendar year QOF Entity makes its initial election to be treated as a QOF in a month after June, the testing period for that year will be the last day of the QOF’s taxable year. For purposes of determining values, if the QOF has audited financial statements, it must use the asset values reflected therein. If no audited financial statements are prepared, the cost of the assets will be used for determining the 90% test.

Failure to comply with the 90% test, unless due to reasonable cause, will subject the QOF to a penalty equal to the federal underpayment interest rate multiplied by the excess of 90% of the QOF’s aggregate assets over the aggregate amount of QOZ property held by the QOF for each month the QOF fails the 90% test.

Types of QOZ Investments:

As indicated in the summary above, an investment in a Qualified Opportunity Zone can be made either in tangible property located in a QOZ or as equity contributed to a business operating in a QOZ. The requirements for each of these types of QOZ investments is set forth below:

QOZ Property:

QOZ Business Property: QOZ Business Property includes tangible property used in a QOF’s trade or business if:

- The property is acquired by the QOF after December 31, 2017 from an unrelated party (i.e. no more than 20% common ownership);

- The original use of the property commences with the QOF or the QOF substantially improves the property; and

- During substantially all of the QOF’s holding period for such property, substantially all of the use of such property is in a QOZ.

The most significant and in some cases challenging portion of this 3 part test to qualify as QOF property relates to the original use requirement and will come into play predominantly in the real estate development or expansion markets.While QOF property can include any tangible property, the original use issue will arise most frequently with the purchase of existing real estate in a QOZ, where the original use of the property does not commence with the ownership by the QOF (or Qualified Opportunity Zone Business), and in this context, such property must be substantially improved in order to qualify as QOZ property. The rules relating to substantial improvements are as follows:

- Where a building and land are purchased together, the cost of land is not included in the QOF’s adjusted basis in the building and the QOF is not required to substantially improve the land.

- Property purchased by a QOF that is already in use (including Real Estate) is substantially improved by the QOF if, during any 30-month period beginning after the date of acquisition, capital improvements (additions to basis) are made to the property in an amount that is more than the QOF’s original cost basis in such property at the beginning of the 30-month period.

In the case of the investment in unimproved or vacant land, the current interpretation is that the original use provision commences with the development or improvement of the land into a property type (i.e industrial, retail, distribution, etc.).

The impact of the substantial improvement requirements on real estate investments means that for any investment in QOZ property where a building already exists, an additional investment in the form of improvements, additions, expansions or rehabilitations equal to or greater than the original cost of the building will be required in order to qualify the property as QOF property.

QOZ Businesses:

QOZ Business Conducted by QOF Subsidiary: While the QOF may hold a direct interest in the qualifying QOZ property, it may also own an interest in newly issued partnership interests or stock of a corporation where such entity is conducting a Qualified Opportunity Zone Business (QOB). Where a QOF invests in a QOB, the requirement imposed on the QOF with regard to holding 90% of its assets in QOZ property is reduced to 70% at the QOB subsidiary level.

As currently interpreted, this means that the QOB subsidiary is only required to qualify 70% of its assets as QOZ property, with the net effect being that where a QOF establishes a QOB partnership or corporation to conduct the Opportunity Zone business, after applying the asset requirements at the QOF level (90%), the total investment required in actual QOZ property will be reduced to 63%.

In addition to the QOZ property threshold for QOB’s above, the business is subject to four additional requirements which include:

- 50% Active Income: At least 50% of the total gross income of the QOB is derived from the active conduct of the QOB.

- Substantial Assets Used in Business: A substantial portion of the QOB’s intangible property is used in the active conduct of its business. This has yet to be further defined.

- 5% Limit on Financial Assets: Less than 5% of the aggregate adjusted basis of the QOZ property is nonqualified financial property which includes debt, stock, partnership interests, options, futures and forward contracts, warrants, notional principal contracts, annuities and other similar properties to be identified in regulations.

- Ineligible Qualified Opportunity Zone Businesses: A QOB may not operate certain “sin businesses” which include a golf course, country club, massage parlor, hot tub facility, suntan facility, race track or other facility used for gambling, and any store that sells alcohol for consumption away from the premises. At present, there is no restriction on leasing real estate to such businesses so long as the QOB is not operating such business itself. An example of the types of businesses that could qualify as a QOB include manufacturing businesses, office buildings, rental housing, mixed-use developments, parking facilities, retail-grocery stores (limited liquor sales), research facilities, hotels, restaurants, or health facilities.

Where a QOF invests in a QOB subsidiary, especially where the QOB involves developing or improving real estate property, the proposed regulations have provided certain allowable working capital safe harbors for such QOB’s in order to avoid violating the income or asset requirements listed above. Further guidance from the Treasury Department will be required to address various unanswered questions relating to QOB’s, including for example whether placement of a business that operates primarily thru the internet can conduct its global business from an Opportunity Zone and still qualify for the QOF benefits.

Examples:

Investment in QOZ Property (real estate):

In 2019, Sam, a real estate investor sells his interest in an office complex for $25,000,000 which he had purchased in 2008 for $15,000,000. The long term capital gain of $10,000,000 would be subject to federal capital gains tax of $2,380,000 (includes 3.8% NIIT). To defer the tax on the gain, Sam rolls the entire gain of $10,000,000 into a QOF (through an LLC partnership) which will invest in an block of properties located on the south side of Chicago with the purpose of redeveloping such properties into a mixed use of office, retail and residential housing. All of the building improvements that exist on the property will be retained (not demolished) but will be rehabbed, expanded and improved. The value of the land associated with these properties is $1,000,000.

In order to overcome the original use requirement, Sam must make substantial improvements to the properties in an amount equal or above $9,000,000 ($10,000,000 invested less $1,000,000 of Land). Assuming such improvements are made, Sam will be able to defer the tax on the $10,000,000 gain until the earlier of December 31, 2026 or the date he sells his interest in the QOF. He keeps his investment in the property and on his 2026 income tax return, he will report $8,500,000 of capital gain income and pay federal tax of $2,023,000.

Following the redevelopment of the property, Sam will receive rental streams of income from the various properties and will pay tax on such net income each year as he would have if he had not invested in a QOF. In 2030, when the value of the QOF properties are $30,000,000, Sam sells his interest in them and recognizes an economic gain of $11,000,000 ($30,000,000 sale price less $19,000,000 of cost basis) but for tax purposes, he will have held the property for more than 10 years and will increase his basis to the fair market value of $30,000,000 at such time and therefore, will recognize no taxable gain on the sale of the QOF properties.

Investment in QOZ Business:

Jim has just sold his entire manufacturing and distribution business for $100,000,000 and realized a long term capital gain of $80,000,000. He is not yet ready to retire and wishes to do something good for his hometown that has been economically distressed for many years and has recently qualified as an Opportunity Zone. On August 31, 2019, Jim decides to invest $25,000,000 of his capital gain in a new warehouse and distribution business. He purchases the vacant land and builds a series of warehouses and distribution centers that will employ 400 people. The $25,000,000 that Jim rolls into the QOB will not be subject to federal capital gains tax in the same manner as described in the example above.

Assuming Jim does not sell his interest in the business until 2035 for $40,000,000, his tax consequences would be as follows:

2019 – 2035: Jim recognizes net income or loss from operations of the QOZ business on his tax return.

2019: Jim recognizes and pays tax on $55,000,000 of long term capital gain not invested in a QOF. The remaining $25,000,000 is tax deferred since it was invested in a QOF.

2024: Jim increases his basis in the QOZ business by $2,500,000 reflecting 10% of his gain.

2026: Jim increases his basis in the QOZ business by an additional $1,250,000 (5% of gain).

2026 Tax Return: Jim recognizes long term capital gain of $21,250,000 ($25,000,000 less $3,750,000 of additional basis).

2035 Sale: Jim realizes an economic gain of $15,000,000 but increases his basis to the fair market value at such time which is $40,000,000. As a result, Jim does not recognize any additional capital gain upon the sale of the business in 2035 since he held the QOZ business for more than 10 years.

Comparison to Like-Kind Exchanges of Real Property:

For the real estate markets, the availability of deferral through the use of like kind exchanges (LKE’s) under Section 1031 was preserved in the recent tax legislation (while eliminated for all other types of property) and remains a viable planning strategy, especially for more permanent real estate investors. There are however some distinctions between LKE’s and QOF’s that should be considered by investors contemplating reinvestment of gains from real estate and include the following:

- QOF’s do not require reinvested gains to be of like kind property or limited solely to real estate type property (i.e. gains from sale of real estate reinvested in QOZ business).

- QOF’s do not require full reinvestment of both the original investment/principal and the gain in the new QOF investment.

- LKE’s do allow for indefinite deferral, especially for institutional investors in real estate, by continuing to roll over gains.

- LKE’s do not require substantial improvements in already existing property as do QOF’s.

- QOF’s can provide permanent deferral of tax (up to 15%) on gain reinvested and potentially 100% of gain on QOF appreciation while LKE’s will eventually pay tax on all gains.

For the professional or institutional real estate investor, LKE’s may remain an attractive alternative for deferral of gains assuming they continue to roll over their investments and gains into new properties indefinitely. However, an unanticipated early exit from a 1031 property could change the economics when compared to having invested in a QOF so investors should realistically consider their sale and exit plans before committing to one or the other strategies.

State Tax Implications:

The impact of the benefits derived from investing in a QOF from a federal income tax perspective will be reflected in the income recognition by the QOF investor for the year in which the gain is deferred, recognized or eliminated. Since most states conform to the federal tax treatment with regard to income recognition, with the exception of states that apply modifications to federal adjusted gross income, the benefits associated with the QOF investment should result in additional state income tax savings as well.

Conclusion:

While some of the rules and regulations relating to this new investment opportunity are still being drafted by the Treasury Department, with a set of regulations addressing the rollover of gains from one QOF to another QOF expected to be published soon, the investment and real estate markets have not paused in their efforts to capitalize on what the U.S. Treasury projects could be a $100bln industry.

With a projected $6 trillion in unrealized gains being held by U.S. taxpayers, such a tax savings opportunity that allows both deferral and permanent elimination of tax while assisting underdeveloped communities may warrant further consideration when reviewing your investment strategies. Members of the Duggan Bertsch team are available to assist you in evaluating and pursuing such investments.

United States

Qualified Opportunity Zone Map

- Despite the low-income community requirements for Opportunity Zones, many well-known emerging markets have made the list. As these neighborhoods have already begun to attract the attention of institutional funds and are transitioning into vibrant live-work-play neighborhoods, the location risk for prospective investors is substantially less compared with investments in less well-known areas, further away from urban cores.

- The designation of these QOZ’s are represented by 77% metropolitan vs. 23% non-metropolitan tracts where approximately 38% fall in urban zones, 22% in suburban regions and 40% in rural areas.

- The above map as well as other detailed information regarding QOZ’s is available on an interactive basis at https://www.cdfifund.gov/Pages/Opportunity-Zones.aspx.

- Additional QOZ information/data can be found at : https://eig.org/opportunityzones;